Shipping through the Strait of Hormuz has plunged to near standstill levels amid ongoing Middle East tensions, raising concerns over global oil and gas flows. Analysts warn that such a sharp decline could have immediate repercussions on energy markets and shipping costs worldwide.

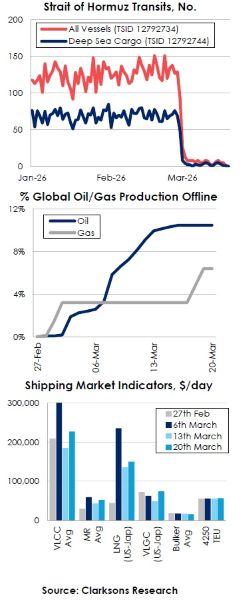

In a statement issued by Clarksons Research summarizing data as of March 23, Steve Gordon, the firm’s Global Head and Managing Director, said ,that vessel transits through the strait remain approximately 95% below pre-conflict levels. Over the past week, an average of four ships per day passed through the waterway, compared to around 125 daily transits before the conflict. Of these, 75% were outbound from the Gulf.

Clarksons estimates that around 10 oil tankers, carrying approximately 12 million barrels, transited the strait over the past seven days. This compares with a typical weekly flow of about 250 vessels transporting roughly 300 million barrels.

A limited number of very large LPG carriers continue to transit the strait, with two recorded on the previous day and two Indian-linked vessels passing through on March 23. Overall LPG carrier movements remain around 80% below normal levels.

Energy Flows and Market Impact

Meanwhile, crude exports from Yanbu have increased to approximately 4 million barrels per day, up from 1 million, with the potential to rise to 5 million barrels per day. Around 40 very large crude carriers (VLCCs) are currently waiting or en route, while market dynamics continue to support long-haul oil and gas exports from the United States.

Clarksons data indicates that approximately 10% of global oil supply and 6% of gas supply are currently offline, alongside 3% of global refining capacity.

Inside the Gulf, excluding locally trading vessels, there are an estimated 1,100 ships representing 37 million gross tonnage and a value of around $30 billion. This includes roughly 300 oil tankers, accounting for 6% of global crude tanker capacity (including 8% of VLCCs), as well as 4% of product tanker tonnage, 4% of VLGC capacity, and smaller shares of container ships and bulk carriers.

Despite reduced cargo volumes, vessel charter rates across tanker and gas segments remain elevated, supported by mitigating market factors. Current earnings are estimated at $227,000 per day for VLCCs, $52,000 for medium-range tankers, around $150,000 per day for LNG carriers, and $74,000 for VLGCs.

Bulk carrier earnings remain steady at approximately $15,000 per day, while container freight rates have edged higher, though they remain well below levels seen during the COVID-19 period.

The cost of transporting crude oil has also risen, with shipments from the U.S. Gulf to Asia now averaging $10 per barrel, up from $5 per barrel at the start of the year.

Fuel costs have surged amid supply shortages, with very low sulfur fuel oil (VLSFO) in Singapore reaching around $1,000 per tonne, more than double early-year levels. Clarksons data shows that average container vessel speeds have declined by approximately 2% so far in March.

Prior to the conflict, the Strait of Hormuz accounted for around 20% of global oil supply flows, facilitating major shares of crude, LNG, LPG, and global trade volumes.

Robban Assafina is now on WhatsApp channel. Click Here